We’re excited to introduce you to the always interesting and insightful Diane Moca. We hope you’ll enjoy our conversation with Diane below.

Diane, thanks for taking the time to share your stories with us today We’d love to have you retell us the story behind how you came up with the idea for your business, I think our audience would really enjoy hearing the backstory.

Having my first baby was overwhelming, and I was unsure how I would continue in my demanding career as a television reporter while navigating my new role as a mother. I was thrilled when I negotiated to work two days a week as a reporter at the TV station while spending the rest of the time with my little boy, who was eventually joined by a sister two years later. I had no idea how difficult it would be to find the right child care. I tried a daycare, a foreign nanny, an agency, college students, a former nurse, and neighborhood caregivers. After 12 different child care providers in four years, I was frustrated by the time and effort I had to spend searching, vetting and hiring — only to have a sitter leave after a few months because they couldn’t accommodate my changing part-time schedule. When I finally found my forever nanny who stayed with our family for eight years, it relieved my stress, guilt and self-criticism.

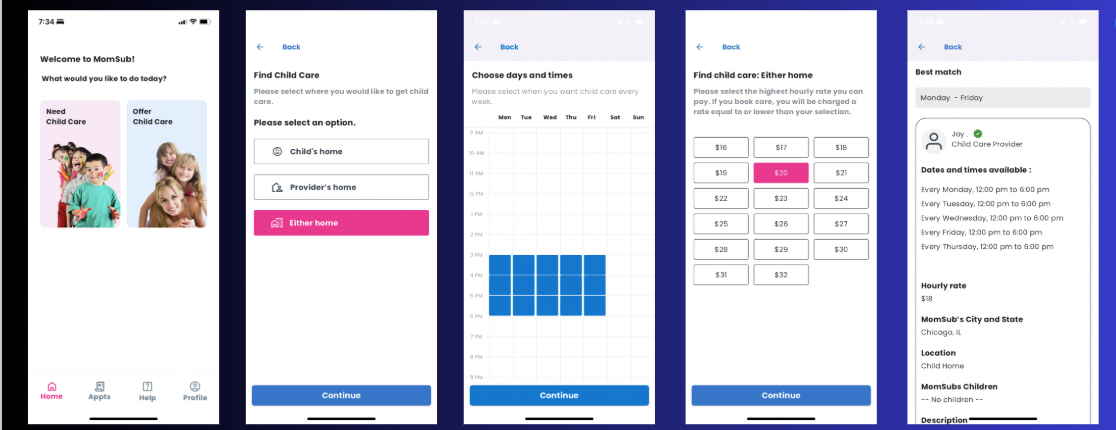

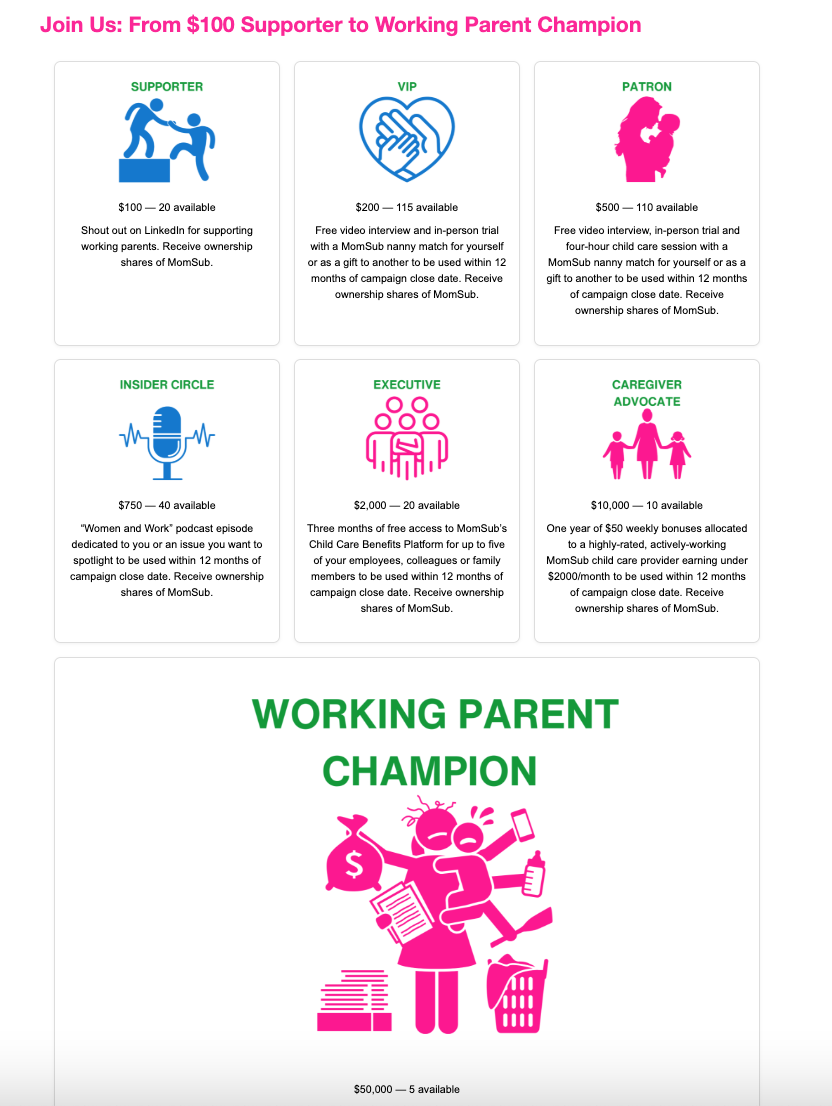

Because of the trusted, reliable and stable care of my nanny, I was able to start a business while maintaining my journalism career and being a hands-on parent. I created my Working Mom Warrior YouTube channel to interview women about their dilemmas. As I heard stories of child care struggles over and over, I decided to use my entrepreneurial skills to develop an affordable and comprehensive child care service. I designed MomSub to be more than just a managed marketplace that connects parents and child care providers. MomSub handles the full logistic and mental load of finding and managing child care – from advertising and interviewing to screenings and negotiations to coordinating schedules and arranging backups. MomSub is on a mission to prevent 2 million women from leaving their careers because of child care challenges!

![]()

Awesome – so before we get into the rest of our questions, can you briefly introduce yourself to our readers.

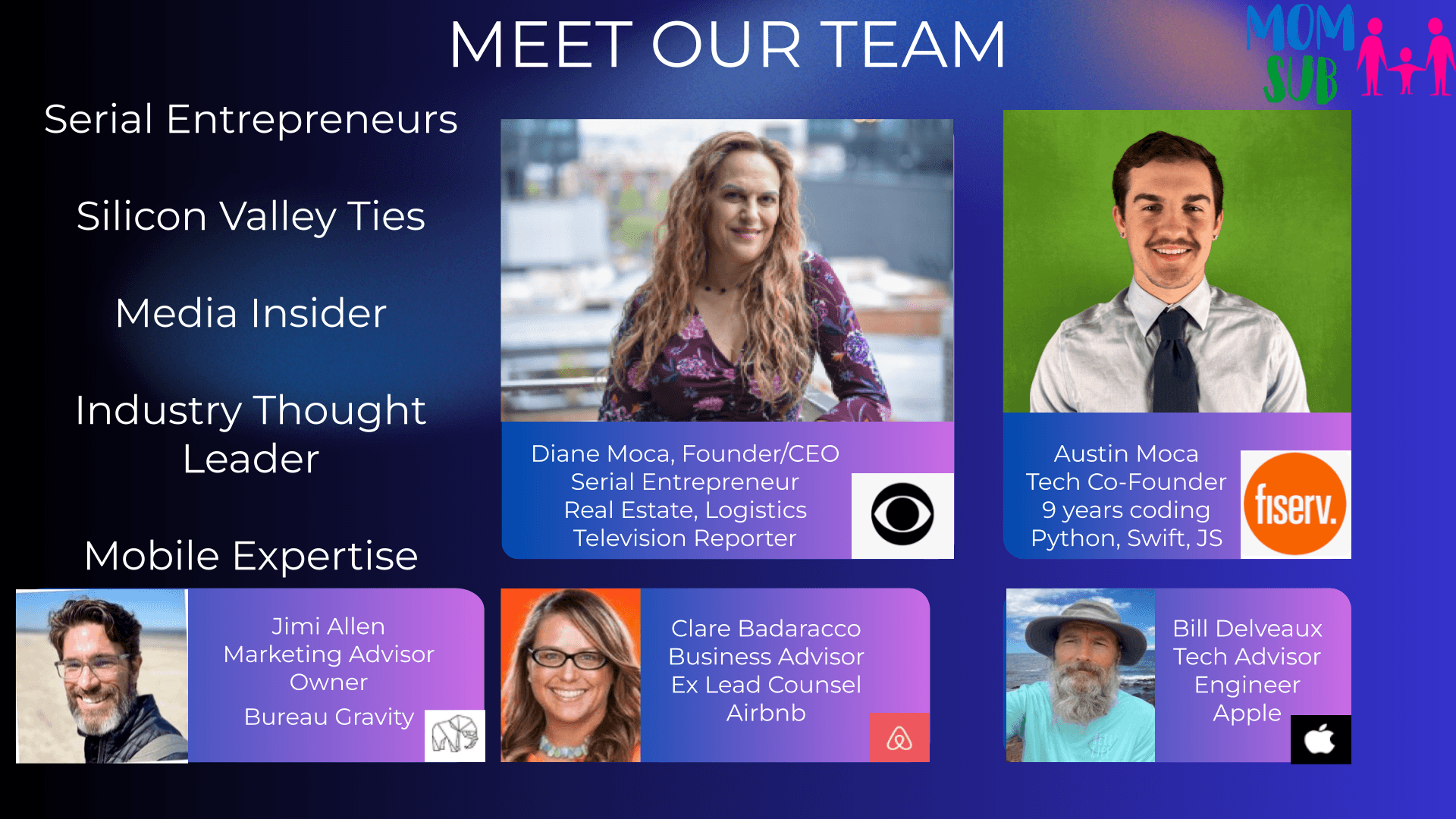

I’m Diane Moca, and I’m a journalist, mother, wife and serial entrepreneur. Like so many working moms, I struggled with child care challenges during my career as a CBS television reporter. After starting and growing a real estate company and buying and running a birthday sign business, I launched MomSub, an affordable and comprehensive child care service. MomSub handles all the work of finding and managing the ideal part-time or full-time nanny, from conducting interviews to running background checks to arranging backup care. My mission is to eliminate the stress working moms experience when they spend hours contacting sitters (who end up canceling) or weeks trying out nannies (who turn out not to be the right fit). Other child care apps charge parents a subscription fee for a list of candidates who may not even respond. It’s like Uber giving you a list of 30 drivers names and numbers and telling you to call them all and get one to pick you up. Instead, MomSub uses technology and video interviews to match a parent to their ideal child care provider who fits their location, schedule and budget. By handling the vetting and negotiating, MomSub confirms the nanny match is interested and available in the role. MomSub provides the comprehensive search services of a nanny agency for a fraction of the cost, and also manages weekly care to resolve conflicts, coordinate schedule changes and arrange backup providers. We are proud when working moms tell us they no longer worry they will have to leave a career they love because of child care challenges.

Let’s move on to buying businesses – can you talk to us about your experience with business acquisitions?

I never studied business in school or had dreams of being an entrepreneur. My passion has been journalism ever since my first internship in a television newsroom. But I’ve always been open to other opportunities, including business ideas that I didn’t dismiss even though they seemed so distant from my skills and interests.

I first learned about business from Robert Kiyosaki after listening to his book “Rich Dad Poor Dad.” My husband and I loved his messages so much we got his board game Cashflow as a Christmas present for our kids when they were 14 and 12 years old. The kids loved it even though it required a lot of math and strategic thinking, and we played it every night of winter break.

After more than a week of Cashflow game sessions in which we all bought fictional commercial properties and businesses, I wanted to show them some real life opportunities. I went on Craigslist and surprisingly found an entire section of small businesses for sale. They were all so inconceivably expensive to us that I wasn’t sure how to use them as a real life example. Then I got an idea to send messages to the owners asking if they would provide seller financing as a purchasing mechanism, a strategy I learned as a result of buying rental houses after following Kiyosaki’s lessons in his classic book. I sent this message to about 20 sellers, and one responded that he would consider such an offer.

I decided to see if we could arrange a meeting, so I could show my kids how this really works. It turns out his business was run by his entire family. His wife and kids helped. He would be happy to meet me with my husband and our kids at his house.

My kids were over the moon with excitement when I explained that we were going on a real life meeting to talk about buying a business like in the game Cashflow. I told them we weren’t really going to buy the business, but they would learn about negotiating and structuring a deal in real life. (I did bring my checkbook just in case, but I had no intention of using it.)

We met the couple in their family room. They were great people. They explained that the business delivered yard decorations, like flamingos, to help people celebrate special occasions like birthdays. They said they bought this business from another man, and he had offered a payment plan for the purchase of the business. So they didn’t mind offering this to us.

I had done some previous due diligence on the business and industry, though there was not a lot of information available. I was skeptical of the revenue projection the owner described and shared that with him. My kids were wide-eyed watching me pull no punches and asking direct questions. Why would someone get rid of a business that was profitable?

The owner said the business required someone to deliver the signs between midnight and 6 am, so the recipient was surprised in the morning. He originally got the business for his college-age son to earn money, because he said he could make the same amount of money in a couple hours of late-night deliveries that he could make working 20 hours a week at a fast food place. But his son had recently moved to the city and gotten a full-time job, and now the man was stuck driving around at 2 in the morning delivering signs. And he didn’t want to do that anymore. He had enough income from his real estate endeavors that he could let this income go. It all seemed very reasonable.

I was actually starting to consider this as a real business endeavor. I had never purchased a business before, but the value of doing it had been drilled into my head after a couple weeks of playing Cashflow. Our kids were not old enough to drive, but they would be in a couple years. They could help us with social media marketing and sending emails to customers.

We really needed the extra money, but we couldn’t afford a down payment. We had gone into debt to buy rental properties right before the real estate market crashed, and we had spent years trying to pay off the credit cards we had used to rehab the properties, which stopped making money during the Great Recession. We were just starting to pull out of that financial hole, and here I was thinking about digging us a new hole.

But I’ve never been afraid of financial risk, because I usually feel like I don’t have much to lose — especially when you don’t have to pay anything up front.

So I told the seller it sounded intriguing, but I was worried about the ups and downs of the business revenue. Then his wife pulled up some reports from a credit card processor called Square that I had never heard of. I examined them. They looked pretty official. They showed much more income per month than the limited expenses the couple described: gas, web hosting and a dedicated phone number.

I told him I was concerned that we were new to the business, and we wouldn’t generate the same income that they were producing, especially since they were not doing that consistently every month. We could not possibly commit to payments that were potentially more than the revenue. We had no extra income; in fact we were self employed and had inconsistent income. We had not dug ourselves fully out of debt. We would be buying this business to boost our finances, not strap them.

I offered payments that were half of what the seller proposed. He said he would consider that but needed to know how much down payment we were offering. I told him we had none. He said that would not work. As someone who had learned about business through real estate investments, I knew it was dangerous to do any financial dealing with someone who has no skin in the game. He knew this too. So I offered him a small down payment. He still said no way.

I kept thinking that after we paid off the seller-financed business loan, this would be a nice way to generate extra income. I kept thinking how much fun and educational it would be for the kids to help us with this business.

So we went back and forth with several proposals and offers and counter offers, all while his spouse and kids and my spouse and kids watched. I told him I couldn’t pay him more than we had in the bank. I told him if I was going to put money down, I needed a lower purchase price and a lower monthly payment.

I wasn’t really sure what the business was worth. I knew that there were two main points to a financial negotiation — price and terms. If you get your way with terms — long-term payment plan instead of full upfront cash payment — you don’t usually have much wiggle room on price.

But I didn’t come to the house to buy a business. I came to teach my kids some lessons, so I wasn’t worried about killing the deal. It would all be a learning experience. Still, a part of me thought this would be a great opportunity. So I offered an affordable purchase price as a counter, and the owner said he would take that price if I wrote him post-dated checks for every monthly payment for a year and a down payment that equaled the balance in my bank account. He was only willing to agree to the deal if I paid the down payment right then.

I thought about my bank account, which was my cushion for when our rental properties needed repairs or when we had to pay mortgages during vacancies. But I reasoned in my head that we would earn back that down payment through this new business.

I got out my checkbook to check the balance in my register. That’s when my ability to negotiate ended, but I knew that. I was ready to commit to this. My kids were excited, and my husband was a little nervous. But he knew I handled the finances, and he always trusted me that I made it all work out. We hadn’t become homeless yet!

I asked the seller to show me a few more things about the business, like how to access the special phone number and the website dashboard. Then his wife got out all their files and records and usernames and passwords and handed them to me. The seller walked my husband and kids out to the garage to see the signs and proudly brag how his wife had just repainted them all. They even had the extra paint and supplies. I was hooked.

We both decided if we were going to do this, it needed to be right then. He drafted a short contract on his computer, as I stood over his shoulder and suggested wording and insisting on including certain clauses. We signed the contract, and I wrote all the checks, each dated on the first of the month for the rest of the year. We took all the signs and paperwork and supplies and materials and loaded them in our van. We shook hands, and I hugged his wife. She told me to call if we had any questions or issues.

We did have to call a few times over the next year, to fix issues with the business phone number or website and even to delay deposit of my check one month when my account was short.

Before we left, his wife gave me a lot of wonderful pointers about the business that were critical. Her descriptions were actually far more important than the hour or two of negotiating that got my adrenaline pumping. She said their sales came from people who found their website and called the phone number on it. She said to be successful in this business you have to answer your phone. All. the. time.

She said she took orders all different times in all different places. She took one on a napkin at a restaurant once. I always felt that responsiveness was one of my strengths. I knew I would be good at this aspect of the business, taking the calls day and night no matter what I was doing.

They also said to not be afraid to ask for the standard price and to charge more if the house was far away, because of course it would take more time and more gas to deliver and pick up the display on two separate days. They said people who were looking for a deal wanted to negotiate, and we should only adjust the pricing slightly but not so much to eliminate the profit.

One of the best things she said was how much she loved the business and would miss it, because everyone who called was happy because they were celebrating something — a birthday, new baby, anniversary. It was easy to be excited with them about the upcoming occasion that a friend or family member was celebrating. I never forgot all of those insights about this business.

We were all pretty excited when we got home. The kids jumped right into the social media pages for the business, adding information to Facebook and creating new profiles for Twitter and Instagram. And just like the owners had said, I sometimes got calls when I least expected them — and I stopped what I was doing and answered questions and took orders. I would write them down on all sorts of scraps of paper in my purse, sometimes in the grocery store. We finally created an order form a couple years later, and I kept a stack of those forms in my purse, in my nightstand, and in my desk.

The first year, we had (barely) enough revenue from sign deliveries every month to make the business loan payment to the seller. After the second year, we had paid off the business loan to the seller and just had to cover monthly expenses like gas. We were finally profitable!

Over the years, we’ve had to replace some supplies and buy some additional ones. But just as the sellers promised, the business doesn’t have too many expenses if you do the work yourself and maintain a consistent 75% sales conversion, which I did. We used the revenue from the business to pay for our kids’ music lessons, travel sports and other activities.

I eventually learned how to increase the business revenue by paying attention to customers. In addition to the two basic options listed on the website, occasionally someone wanted to combine those two sign displays, and I would offer to do that for far less than the combined cost of both options. One day I suggested to a caller that we had a third option, and on the spot I gave it a name and called it the “deluxe package.” The customer liked that and went with it. I found myself suggesting the third “deluxe” option more often, and I was pleasantly surprised more people were interested. It was more work but more revenue too. I discussed this with a friend who said simply using the word “deluxe” was more enticing to customers who want to think that they are going to provide their loved one with the best — and enjoy a bargain doing it, since the combined deluxe cost was far less than the combined cost of the individual items .

Adding that one word increased my revenue about 50% the first year. It was an amazing business lesson, and one I learned before I even added pictures of the deluxe option to our website. But the most exciting phase of the business came during the most unlikely time – the covid pandemic.

The day after the entire country went into lockdown, my phone started blowing up with people asking about our signs. Many of them were moms wanting to do something special for a child who couldn’t have a birthday party because of the covid quarantine. I was so happy to help them out and find something that would brighten their child’s day amid a very challenging time.

Like I’ve been doing for years, I get excited talking to people about a special occasion. I love celebrating holidays and birthdays, and I’m sure that enthusiasm comes across in my conversations. I know my personality fits very well with this business. I’m very detail-oriented, and I’ve heard from many of my customers that I take the time and focus to get everything just right during that initial and only contact. I do a lot of little things on the phone and then afterwards behind the scenes to make sure everything stays organized and goes right.

This all seems to help me build a quick relationship with each potential customer who calls. During the pandemic, the increase in calls was very exciting to me and my family, knowing we could help so many people and boost our sign revenue at a time when we had to face other lost revenue.

Though we had the supplies to set up multiple displays in one night, we had to boost our supplies and efforts to meet the growing demand without changing our business approach or model. During the first two months of the pandemic, my daughter helped with orders, and my husband and son were out delivering signs every night for 60 days straight. We hired six new drivers to help us. I worked 18 hours a day every day for those two months. I had to learn how to coordinate logistics of picking up and delivering hundreds of different items every night to ensure they all got to the right place. We boosted our sales 5000% month over month. It was exhausting but exhilerating.

We used the profits from those two months to buy every member of my family a car. I got rid of my old car with no heat (which isn’t pleasant in Chicago winters)! My kids each got their first vehicle. My husband got an SUV that he took on a dream “van life” vacation visiting national parks in the west. And I used a portion of the profits to start my next business, MomSub, a child care app that matches parents to their ideal nanny.

Though the intense demand during 2020 eventually subsided, the business now generates 10x more revenue than it did pre-pandemic. Through it all, our little side business has not gone away. We now have a manager who takes orders and handles the logistics of the nightly route and a driver who does the deliveries and pick ups. And Lawn Greeting Cards has a special place in our family’s history as a major project we worked on together. And it all came about because we were open to the power of possibility.

Let’s talk about resilience next – do you have a story you can share with us?

I’m sitting on the couch. My kids are running around in the living room. My husband is talking in the kitchen. I can’t actually hear any words because everything sounds like the “wah waaaaah wah wah wah waaaah” of Charlie Brown’s teacher.

I should get up and play with my kids or help with dinner, but I can’t actually move because I feel as if I am frozen. My mind is blank in a way I have never experienced. I am stuck in every conceivable way.

I stay in this spot for the entire weekend. I don’t move. I don’t talk. I don’t eat. I vacillate in and out of sleep. I am an observer in my life. My family eventually treats me as a piece of furniture. I am an inanimate object incapable of interaction.

There is just one thought that keeps running through my mind like a caption on a screen: There’s no way out.

Six years earlier, life was full of promise. I had a great career I loved as a television reporter, and I listened to audiobooks during my long commute. One day I picked up the book Rich Dad Poor Dad from the library not knowing what it was about or how it would change my life.

I was blown away by the concepts in that book that were previously unknown to me – about wealth, money mindset and passive income. It got me excited to become a real estate investor.

It was the first time in my adult life that my debts were paid off, and I had savings in the bank. I thought that was the smart, safe way to handle my finances until the book taught me that I needed to learn how to make my money work for me.

My husband supported my decision to use our savings to buy a rental house. I spent months researching to find the right deal and more months securing the financing and finding the right tenant. And then it worked just like the book said: the tenant paid the mortgage, and we had an asset.

I thought we had to wait a few more years to save up more money for a down payment to buy another investment property, until I got the audiobook Nothing Down. I learned how to buy real estate even though I had no money. It was the first time in my life I loved shopping, and I went on a shopping spree! I bought eight more rental properties in the next four years – houses, townhouses, condos, even a four-unit apartment building. When they needed repairs, I got credit cards to cover the cost. After fixing up a property to make it worth more, I could do a cash-out refinance to pay off the credit cards. I had been listening to nothing but real estate books for years. I knew all the tricks. Or so I thought.

It was September 2008. I was approved for a refinance and a few days from closing. I needed the cash proceeds from the refinance to pay off a large debt used to rehab the house before the low teaser rate on the credit card expired.

The mortgage broker called to say they were canceling my refinance. I was incredulous. I had experienced some financial challenges with vacancies and overzealous inspectors, but I had managed to pay my bills and keep my credit score in good standing. This must be a mistake.

He said it was happening to all his clients all over the country. He said the markets crashed and the loan industry was imploding. I didn’t understand. This wasn’t in any of the books or courses I had been listening to for years.

I was screaming at him that he was ruining my life because my credit card interest of 3% was going to jump to 13% without this money. He told me to get a loan somewhere else. So I tried. And tried. And tried.

I never had any trouble getting financing before. Now, no one was lending. I began to learn about the market crash and the prediction that mortgages could be hard to get for months.

So I decided to get another credit card, so I could transfer my balance and keep the interest rate low. I had been approved for every credit card I had ever applied for. I had about 20 of them. That’s how I paid to rehab the rental properties. So I applied for one more. Not only was I denied, but I was told my credit limit would be reduced and my interest rate increased.

You can’t do that, I screamed. It was like yelling into the void. The bank didn’t care. One by one, all the banks did it. Within a few months, my interest rates were all up to 29% and my payments were double and triple what they had been.

The rents were barely enough to cover the mortgages and the credit card payments for our rental properties. We were cutting back on our own personal expenses to cover repairs for the properties.

And then my husband and I both lost our jobs.

If we could do gig work to pay for our basics, and the rents could cover the bare minimum for the properties, we could make it through until things turned around in a few months. Or so I thought.

Until the next shoe dropped.

The rents stopped coming in. One by one, many of our tenants, just like us, became part of the statistics – among the 8.6 million people who lost jobs during the Great Recession.

Every day was a stressed-out frenzy of moving money from one account to another to try to stay a step ahead of bill collectors, or meeting with tenants to try to get rent or get them to move out if they could no longer pay.

Somehow I thought I was invincible and could keep it all from crashing down. I had always been able to figure out a solution to any problem. I was a juggler adeptly adding more and more balls in the air – until the day a lightbulb was thrown in the mix that made my world go dark.

I was meeting a tenant to show a vacant property. She walked in, looked around, and laughed.

“You want $1350 a month for this place?”

“Yes, that’s what the last tenant was paying. We usually charge more for the next tenant, but I know things are tight with the economy. So we’re willing to keep it at that rent.”

She laughed again. “I’m not going to pay that if I can go down the street and get a place that’s twice as big and twice as nice for $1000.” And she walked out.

“Wait, what do you mean?” I said, as I ran after her. I watched her walk down the street. I looked up the house she entered. She was right. It was all fixed up; it looked like new. It was big. It was cheap. And then I saw them – so many other houses for rent. Why were they all so nice and renting for such a low price?

I started digging into what was happening in the real estate market and learned that people had been trying for months to sell their homes and couldn’t because the banks were not lending to anyone. So they had no choice but to rent their homes – beautiful homes that had been fixed up to sell and had been burning a hole in their pocket while vacant. So they put them on the market for rent at a low price to get them filled.

I had to lower the price on my rental home, which had tenants for years and was not freshly rehabbed. I eventually got it rented for $900 – less than the monthly mortgage.

This scenario started to repeat over and over at our rental properties.

The real estate I had acquired to bring positive passive income to our family had become negative. The expenses for our assets were now much greater than the income. This was not the game I signed up for.

My husband and I were both journalists still unemployed and desperately trying to find work. No one was hiring. Freelance gigs paid $50 or $100 at a time. We were working around the clock and constantly on edge with each other and the kids, and falling further and further behind every day.

Our real estate expenses and personal expenses were thousands of dollars more per month than our income.

How can this be?

This has never happened.

I don’t know what to do.

There’s no solution to this. There’s no solution. No solution. No way out.

There’s no way out.

That’s all I can think as I walk downstairs like a Zombie and sit on the couch, unable to move.

After a couple days, the noise in the background starts to sound like real words again. My brain is catching a few here and there coming from the TV: Crisis. Mortgage. Default. Foreclosure. Modification. Affordable. HAMP.

The disk spinning in the hard drive of my brain that had slowed to a crawl and almost stopped began to accelerate, slowly and steadily, picking up speed.

Maybe. Maybe there is a way. Maybe there is a way out. Maybe there is a solution.

Modification. Can we modify a mortgage? Two mortgages? All the mortgages?

I’ve overcome a lot of obstacles in life, but by far the most difficult one was climbing back from the devastation of my real estate portfolio.

Completing eight modifications, one short sale and one deed in lieu – plus renegotiating payback of more than $100,000 in debt on two dozen credit cards – caused even more pain than childbirth because it took six years of fighting with banks, red tape, court dates, and thousands of pages of documents in an era when companies would only accept submissions by fax (which had to be fed into my machine one page at a time).

On the other hand, labor with my first child lasted 20 hours but blessed me with a healthy baby the next day.

The early predictions that the real estate and financial markets would rise out of the crash within months were way off. The Home Affordable Modification Program (HAMP) lasted seven years from 2009 to 2016, and that’s how long it took for our real estate income to break even and be enough to cover our real estate expenses again.

My husband and I never found full time employment during that entire period.

I used the last of my credit card limit to pay a mentor to teach me a lease-option real estate strategy that helped us bring in some income while reducing expenses through the modifications.

The long, hard and arduous battle to keep my real estate portfolio (and not become homeless) did not bear fruit in a way I could truly enjoy and appreciate for another 10 years – when we finally regained enough equity on paper to make me realize I had a true safety net.

Why? Why did I put myself through such agony? Why did I spend years losing my temper with my husband and kids so regularly because I was feeling constant pressure that our financial house of cards would one day crumble despite all my efforts?

I hated the thought of losing it all, everything I had worked so hard to get. I hated the idea of not fulfilling my obligations that I had committed to. I hated the image of tenants having to leave their homes because of my financial mess.

And I knew it would turn around some day, and the properties would be worth more. The portfolio would be meaningful in our life.

I had to remind myself that I was resilient, that was my identity, that I had overcome obstacles before, that I could do it again.

Though I considered myself to be resilient, I never considered myself to be a patient person. I realize now I had to have patience to trust that my efforts to improve my situation would pay off eventually. I just didn’t realize how very long it would take. Sometimes it’s better not to know when you’re focused on the fight to survive.

Contact Info:

- Website: https://www.momsub.com/

- Instagram: https://www.instagram.com/momsubapp

- Facebook: https://www.facebook.com/MomSub/

- Linkedin: https://www.linkedin.com/in/workingmomwarrior/

- Twitter: https://twitter.com/WorknMomWarrior

- Youtube: https://www.youtube.com/workingmomwarrior

- Yelp: https://www.yelp.com/biz/lawn-greeting-cards-woodridge-7

- Soundcloud: https://open.spotify.com/show/7neQoQQGoAxblymymEXVum

- Other: https://podcasts.apple.com/us/podcast/women-and-work/id1830784744