We were lucky to catch up with Lisa Pent recently and have shared our conversation below.

Alright, Lisa thanks for taking the time to share your stories and insights with us today. How did you come up with the idea for your business?

I spent nearly 30 years in financial services, senior leadership, enterprise consulting, watching the industry evolve from the inside. And for most of that time, I watched community banks struggle with the same fundamental tension: they’re too important to fail, and too under-resourced to keep up.

When AI started entering the conversation in banking, I didn’t see opportunity first. I saw alarm bells. Not because AI is bad; it isn’t. But the regulatory environment was moving fast, and community banks had almost no infrastructure to respond. The OCC, the FDIC, the Federal Reserve were all issuing guidance. Examiners were starting to ask hard questions. The big banks had teams. Community banks had nothing.

After leaving a senior role at Cognizant, I was doing consulting work when I started noticing a pattern. Every community bank executive I spoke with, COOs, Chief Risk Officers, compliance leads, was saying some version of the same thing: “We know this is coming. We don’t know where to start. And we’re terrified of the exam.”

That was the moment I knew there was something real here.

The problem nobody was solving wasn’t AI itself. It was AI governance, the ability to inventory your tools, assess them against federal guidance, document your risk decisions, and walk into an exam with confidence. The big fintechs weren’t building for $1B community banks. The core banking vendors weren’t moving fast enough. And consultants, myself included, could only do so much. What these banks needed was a product. A system. Something that lived inside their workflow and gave them a defensible answer when the examiner said: “Tell me about your AI risk management program.”

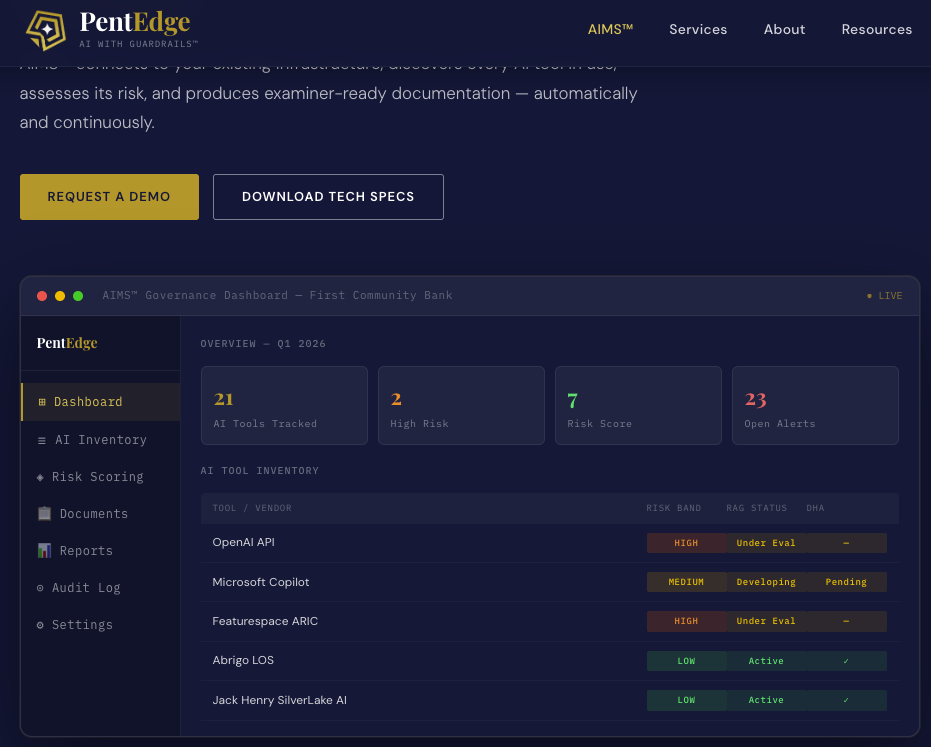

So I built it. AIMS™, the AI Monitoring & Governance System, and founded PentEdge to bring it to market.

Was I scared? Absolutely. First-time founder, self-funded, building a SaaS company from scratch with a development partner in India and a market that didn’t fully know it needed me yet. But I’d spent three decades watching what happens when community banks don’t have the right tools at the right time. I wasn’t willing to keep watching.

What still gets me most excited is that this problem is solvable. It’s not a moonshot. It’s a gap, a real, documented, regulatory gap between what examiners expect and what community banks currently have. And I have the experience, the network, and now the product to close it.

That’s not a startup story. That’s a mission.

As always, we appreciate you sharing your insights and we’ve got a few more questions for you, but before we get to all of that can you take a minute to introduce yourself and give our readers some of your background and context?

I didn’t set out to be a founder. I set out to be useful, and after nearly 30 years in financial services, I finally found the place where being useful meant building something from scratch.

My career started in banking. Twenty-five years of it, working my way through roles that gave me a ground-level understanding of how community banks actually operate: the pressures they face, the relationships that hold them together, the regulatory weight they carry every single day. From there I moved into enterprise consulting, eventually reaching senior leadership at Cognizant, one of the largest technology and professional services firms in the world. I’ve sat across the table from bank executives, regulators, and technology leaders. I’ve helped large institutions navigate major transformations. I’ve seen what works, what fails, and critically what gets ignored until it becomes a crisis.

What kept getting ignored was community banks.

These are the institutions that fund the small business on Main Street, approve the mortgage for the first-generation homeowner, and show up when the big banks won’t. There are thousands of them across the country, with assets ranging from $500 million to $100 billion, and they are the backbone of local economies. They’re also perpetually under-resourced when it comes to technology, compliance infrastructure, and now AI governance.

That’s the problem I built PentEdge to solve.

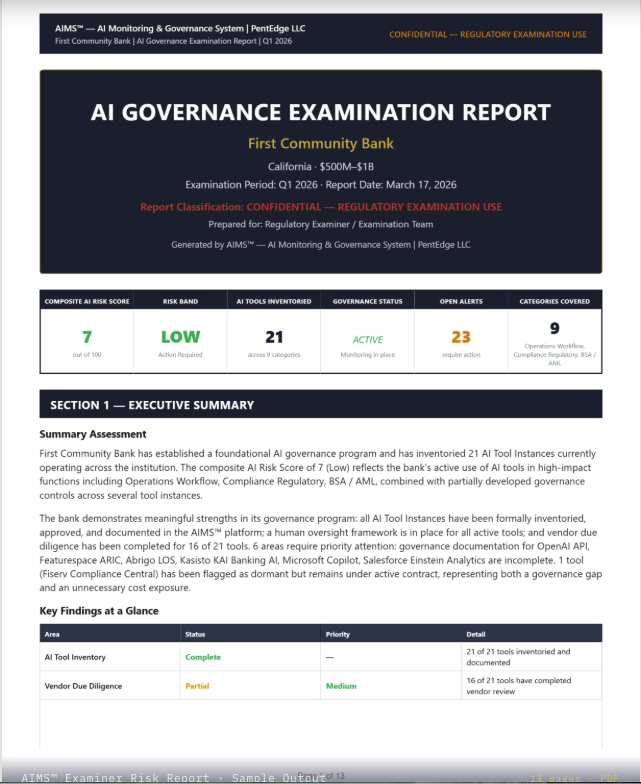

PentEdge is a women-owned fintech company, and our flagship product is AIMS™, the AI Monitoring & Governance System. It’s a SaaS platform purpose-built for community banks and credit unions that need to manage AI risk, meet federal regulatory expectations, and walk into an examiner review with confidence. Think of it as the command center for everything a bank needs to say “yes, we have our AI house in order.” We help them inventory every AI tool they’re using, assess those tools against current federal guidance from the OCC, FDIC, Federal Reserve, and others, document their risk decisions, and generate the kind of board-ready and examiner-ready reports that used to require a team of consultants or didn’t exist at all.

What sets us apart? A few things, but the most important one is this: I’ve lived the problem from both sides. I’m not a technologist who learned banking. I’m a banker who learned technology and that distinction matters enormously when you’re building compliance infrastructure. The language I speak, the workflows I designed, the reports AIMS™ generates, they’re built for the Chief Risk Officer who needs to brief her board on Thursday, not for a developer audience. That’s not an accident. That’s 30 years of accumulated context baked into the product.

I’m also a first-time founder, and I want to be honest about what that means. I launched PentEdge a little over a year ago. I’m self-funded, scrappy, and building this with an extraordinary development partner. I wrote the business plan, closed the partnerships, shaped the product, and brought AIMS™ to its MVP launch — all while learning what it means to build a company from the ground up, in an industry I know deeply but in a role that was entirely new to me. That journey inspired me to write The Courage to Advance, a book about exactly that kind of leap, the ones you take not because the path is clear, but because standing still stops being an option.

What am I most proud of? That I didn’t wait for permission. The market needed this product. Community banks deserve better tools. And I had the experience and the conviction to go build it rather than wait for someone else to.

What do I want potential clients and followers to know? That PentEdge isn’t a startup trying to sell technology to banks. We’re a mission-driven company led by someone who has spent three decades earning the right to sit at this table. When you work with us, you’re not getting a vendor. You’re getting a partner who understands what keeps you up at night, because I’ve been in the room when those conversations happen.

AI governance in banking isn’t optional anymore. The examiners are coming, the guidance is clear, and the community banks that get ahead of it now will be the ones that thrive. That’s what we’re here to help with. That’s what gets me out of bed every morning.

Let’s talk about resilience next – do you have a story you can share with us?

About a year into building PentEdge, I found myself facing something I never anticipated: a dispute over the intellectual property at the core of my business.

I had been working with a partner to develop the early proof-of-concept for what would become AIMS™. The work was real. The vision was mine. But when the relationship deteriorated, so did the clarity around who owned what. And in a technology business, IP ownership isn’t a footnote, it’s the foundation. Without clean IP, you don’t have a product. You don’t have a company.

I’m not going to sugarcoat what that felt like. I had invested significant time, money, and trust. I was a first-time founder who had left a senior corporate career to build something from scratch. The idea that I might have to start over, completely over, was genuinely terrifying.

But here’s what I learned in that moment: panic is just energy that hasn’t found its direction yet.

I made a decision. Instead of fighting over a proof-of-concept that was already compromised, I would rebuild — from scratch, with clean ownership, with the right partner. I reached out to Phil Samuelraj, the CEO of TechJays, who had already been in my corner as an advisor for over a year without asking for anything in return. I told him what happened. I told him what I needed. And we built it again, the right way, with proper agreements, clear IP ownership, and a partnership built on trust rather than assumption.

Was it a setback? Absolutely. Did it cost me time, money, and sleep? Yes to all three. But the product that came out the other side, the AIMS™ platform we launched in March 2026, is cleaner, stronger, and built on a foundation I actually own. And the partnership with TechJays is one I’d put up against any founding team in this industry.

The lesson I carry from that experience is this: the thing that almost stops you is often the thing that clarifies exactly what you’re building and why. I didn’t rebuild AIMS™ because I had to. I rebuilt it because this problem, community banks without AI governance infrastructure, is too important to walk away from over a contract dispute.

Some founders have a clean origin story. Mine has a scar. I’ve decided that’s not a liability. It’s proof that this wasn’t a whim.

Can you tell us the story behind how you met your business partner?

The best business partnerships don’t always start in a boardroom. Mine started at 4am in a boarding line at Chennai International Airport.

I was exhausted, traveling back to the US, waiting to board with the particular kind of patience that only a pre-dawn international departure requires. In front of me was a visibly tired father and a nine-year-old girl who was absolutely, completely, unapologetically awake. She had the energy of someone who had slept twelve hours and eaten a full breakfast. He had the look of someone who had done neither.

She said “pick me up.” He picked her up. She wiggled down. “Pick me up.” He picked her up again. I watched this cycle repeat with the quiet amusement of a fellow traveler who was very grateful in that moment not to be that dad.

Eventually we started talking, the way you do when you’re stuck in a slow-moving line at an hour when conversation feels both impossible and necessary. I learned that his name was Phil Samuelraj, founder and CEO of TechJays, a technology company based in India. I learned that his daughter’s name was Lisa.

Same as mine.

That small coincidence cracked the whole thing open. By the time we boarded, we were no longer strangers. On the flight, Phil slept, deeply, deservedly, immediately. Little Lisa, however, had other plans. She stayed wide awake, watched videos, and kept me company the whole way.

I think about that morning a lot. I didn’t board that plane looking for a business partner. I wasn’t pitching anything. I was just a tired traveler in a boarding line who noticed a dad doing his best. But that chance encounter planted a seed that grew over months of conversation, mutual respect, and a shared belief that community banks deserve better technology into the partnership behind PentEdge and AIMS™.

Phil has been in my corner from the beginning, long before there was a product, a contract, or a reason to be. His daughter, the other Lisa, unknowingly made the introduction.

I’d say she gets some credit for whatever we build.

Contact Info:

- Website: https://www.thepentedge.com/

- Instagram: https://www.instagram.com/thepentedge/

- Facebook: https://www.facebook.com/search/top?q=pentedge

- Linkedin: https://www.linkedin.com/company/thepentedge/

- Other: https://www.linkedin.com/in/lisapent/

Image Credits

Andrew Weeks Photography