We were lucky to catch up with Jonathan recently and have shared our conversation below.

Jonathan, thanks for taking the time to share your stories with us today How did you come up with the idea for your business?

The idea for HomeVest really grew out of my own path through housing and finance. I started out in the banking space, then worked in residential construction, and eventually tried my hand at development. My thinking was simple: if I could just build homes at lower margins, I could make them more affordable. But when I told investors, “I want to sell homes for as little margin as possible in the name of affordable housing,” they weren’t exactly excited. That’s when I realized I was tackling the problem from the wrong side.

Instead of forcing prices down, I needed to help people increase their buying power. That’s when the lightbulb went off: if employers can match your 401(k), why not match your down-payment savings? The very structure already exists—your employer withholds your taxes before you see your paycheck, and your 401(k) is taken out automatically. People don’t fight those systems; they rely on them. So why not use that same, proven mechanism to help people finally afford a home?

From a business perspective, it made perfect sense: workers get a clear path to ownership, employers get a benefit that actually moves the needle on retention, and banks get better-prepared, less risky borrowers. And emotionally, what got me most excited was the vision—families who thought homeownership was out of reach suddenly having a real pathway to their first home. That’s when I knew this wasn’t just an idea worth pursuing—it was an idea worth fighting for.

Jonathan, love having you share your insights with us. Before we ask you more questions, maybe you can take a moment to introduce yourself to our readers who might have missed our earlier conversations?

I come from a background that’s pretty intertwined with housing and finance. Early on, I worked in the banking space and saw firsthand how people manage their money and how financial systems shape their opportunities. Then I moved into residential construction, where I got to see the literal building blocks of homeownership. Eventually, I tried to step into real estate development because I believed if I could build more affordably, I could open doors for more families.

But that experience also taught me a tough lesson: investors aren’t drawn to low margins, even if affordability is the mission. That was the moment I shifted my perspective—from trying to lower the cost of homes to finding a way to raise people’s buying power. That’s what led me to start HomeVest.

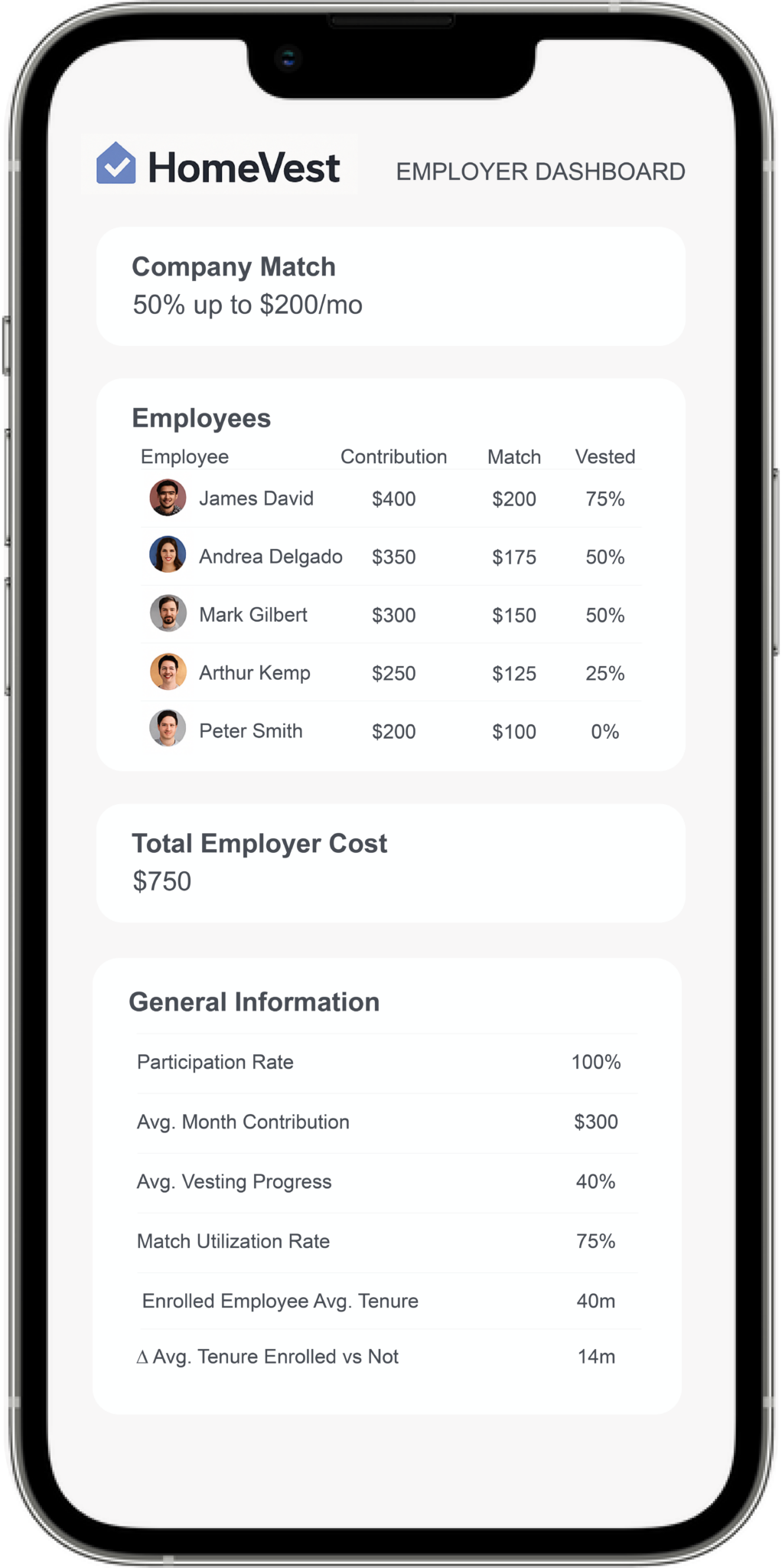

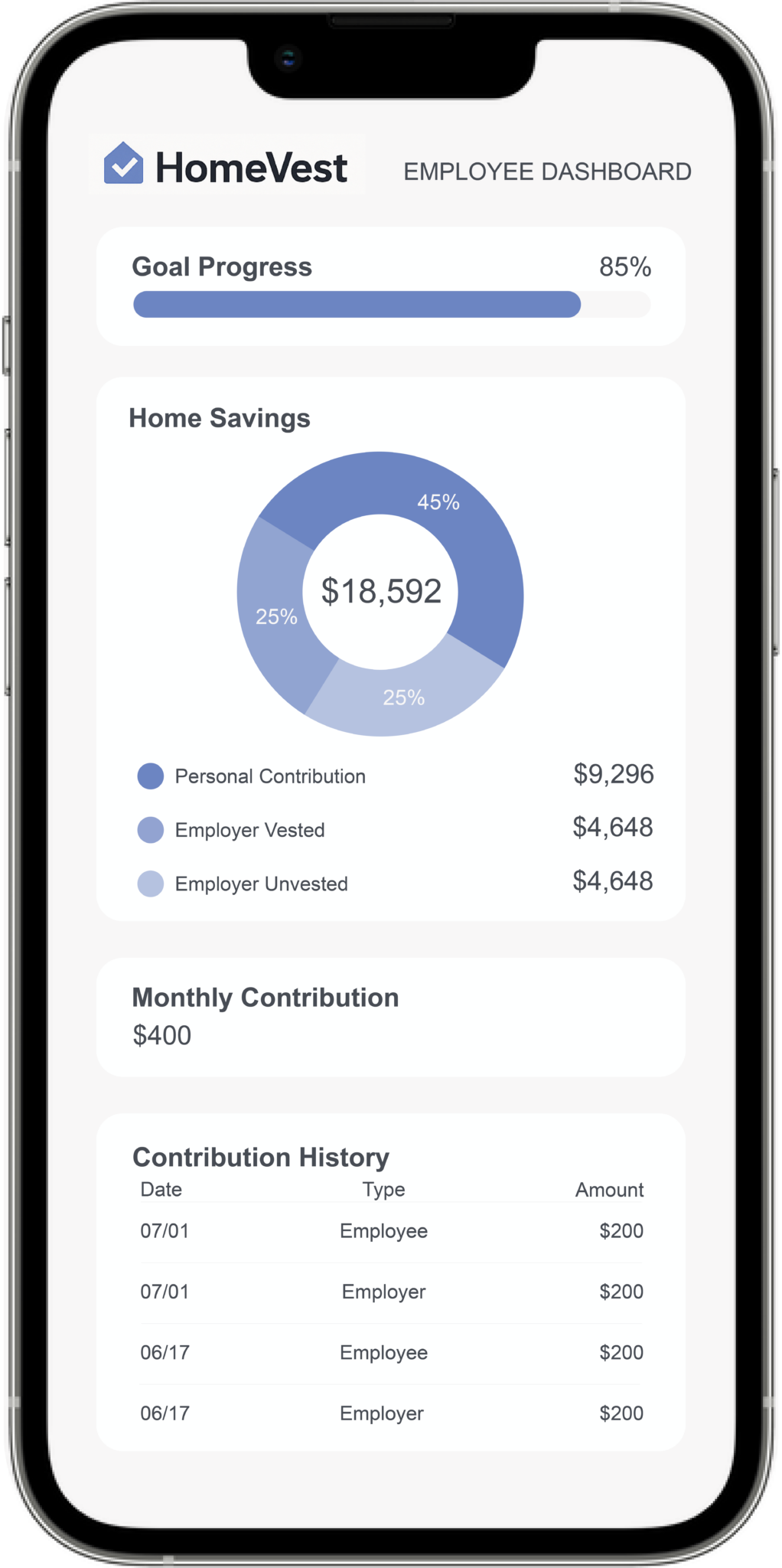

At its core, HomeVest is a benefit platform for employers and employees. We help workers save for a home down payment directly through payroll—automatically, the same way taxes are withheld or 401(k) contributions are taken out before you even see your paycheck. Employers can match those savings just like they do with retirement accounts. It’s a structure people already know, already trust, and now we’re applying it to one of the biggest barriers in their lives: affording a home.

The problem we’re solving is simple but powerful: millions of hardworking Americans are renting for years—even decades—without building wealth, because the hurdle of the down payment keeps them locked out of ownership. By bringing together employees, employers, and banks in one aligned system, we’re creating a benefit that not only helps families but also helps companies with retention and helps banks with better-prepared borrowers.

What sets us apart is that no one else is addressing the homeownership gap in this way. Other solutions nibble at the edges—mortgage products, financial literacy programs—but we’re meeting people where they are: at their paycheck. We’re embedding savings and matching into the same system that already runs their taxes and retirement contributions.

What I’m most proud of is that this idea doesn’t just make financial sense—it makes emotional sense. Homeownership is where 60% of retiree wealth comes from. It’s not just about buying a house, it’s about creating stability, pride, and generational opportunity. Knowing that HomeVest can be the bridge that helps families cross that gap is what drives me every day.

If there’s one thing I’d want potential clients, partners, or followers to know, it’s that HomeVest isn’t about selling a product—it’s about rewriting what’s possible. We want people to see homeownership not as a distant dream but as a reachable milestone, and we’re building the system that makes that possible.

Can you talk to us about how you funded your business?

In the beginning, there wasn’t a big pool of capital behind HomeVest. I started it the way a lot of founders do — by bootstrapping, leaning on my own savings, and putting in sweat equity to get the concept off the ground. My background in banking and construction helped me stretch dollars and build prototypes on a lean budget, and I relied heavily on relationships to test the idea with employers, bankers, and community leaders before we ever thought about outside funding.

That scrappy start was important, because it forced me to really validate the problem. I couldn’t just throw money at branding or infrastructure. Instead, I had to prove that this model — payroll-based savings with employer matching — was something both employers and employees wanted. Once I started hearing “yes” from both sides, I knew it was time to think bigger.

So far, the capital has come from me, my time, and my commitment, but we are now preparing to raise a funding round to scale. The structure works, the interest is there, and now it’s about speed and reach. Scaling HomeVest means more employers on board, more families saving, and more banks ready to partner — and that requires the kind of capital that accelerates growth.

For investors reading this, we see HomeVest not just as a benefits platform, but as a chance to reshape financial wellness in America. If you share that vision — that homeownership should be accessible to millions more families — we’d love to talk.

![]()

What’s been the best source of new clients for you?

So far, the best source of new clients has been relationships and community. I’ve been very intentional about showing up where employers, bankers, and HR leaders are — whether that’s chambers of commerce, networking events like 1 Million Cups, Greater Dallas Hispanic Chamber of Commerce or even informal conversations with people in my network. A lot of our early traction has come from someone saying, “You need to talk to Jonathan about this homeownership benefit,” and that personal introduction opened the door.

Press and word of mouth have also started to play a role. When people hear “401(k) for your first home,” it clicks immediately, and they want to learn more. That clarity in the message has made it easier for people to spread the word on our behalf.

Over time, we know the best long-term source of clients will be partnerships — with banks, benefit platforms, and large employers who can roll this out at scale. But I think what sets us apart right now is that we’re still very grassroots. We’re talking directly to people, hearing their stories, and then working backwards to make sure HomeVest solves their pain. That personal touch has been our best “marketing channel” so far.

Contact Info:

- Website: https://tryhomevest.com