We caught up with the brilliant and insightful Josh Williams a few weeks ago and have shared our conversation below.

Josh, appreciate you joining us today. So let’s jump to your mission – what’s the backstory behind how you developed the mission that drives your brand?

In 2023 I was unexpectedly part of a mass-layoff from a company I loved and had been with for 7 years. My wife and I had a 4yr old and a 5mo. old at home. For many, this type of thing could have meant severe hardship, a forced selling of the house and general financial ruin. But for us it was more like driving through a huge pothole. We didn’t expect it, definitely felt it, but it didn’t break anything or upend our life because of the strong personal finance foundation we had build for ourselves over the previous 12 years.

Its this resilience that I want for others. I love helping others, connecting with people and creating community. I’m a detail oriented, data and finance nerd that loves extreme sports especially snowboarding in Tahoe.

My wife got the same bug to connect and help and followed her calling into education where she is a Board Certified Behavior Analyst with a masters in Human Behavior. She works with special education students from a broad spectrum of backgrounds and disabilities to understand what is driving a behavior and develop interventions to change that behavior.

When I was laid-off we were faced with a choice. Continue working hard for someone else with the uncertainty of being laid-off again or use our backgrounds and create our own business directly in alignment with what we value. Working hard, being kind, and helping others.

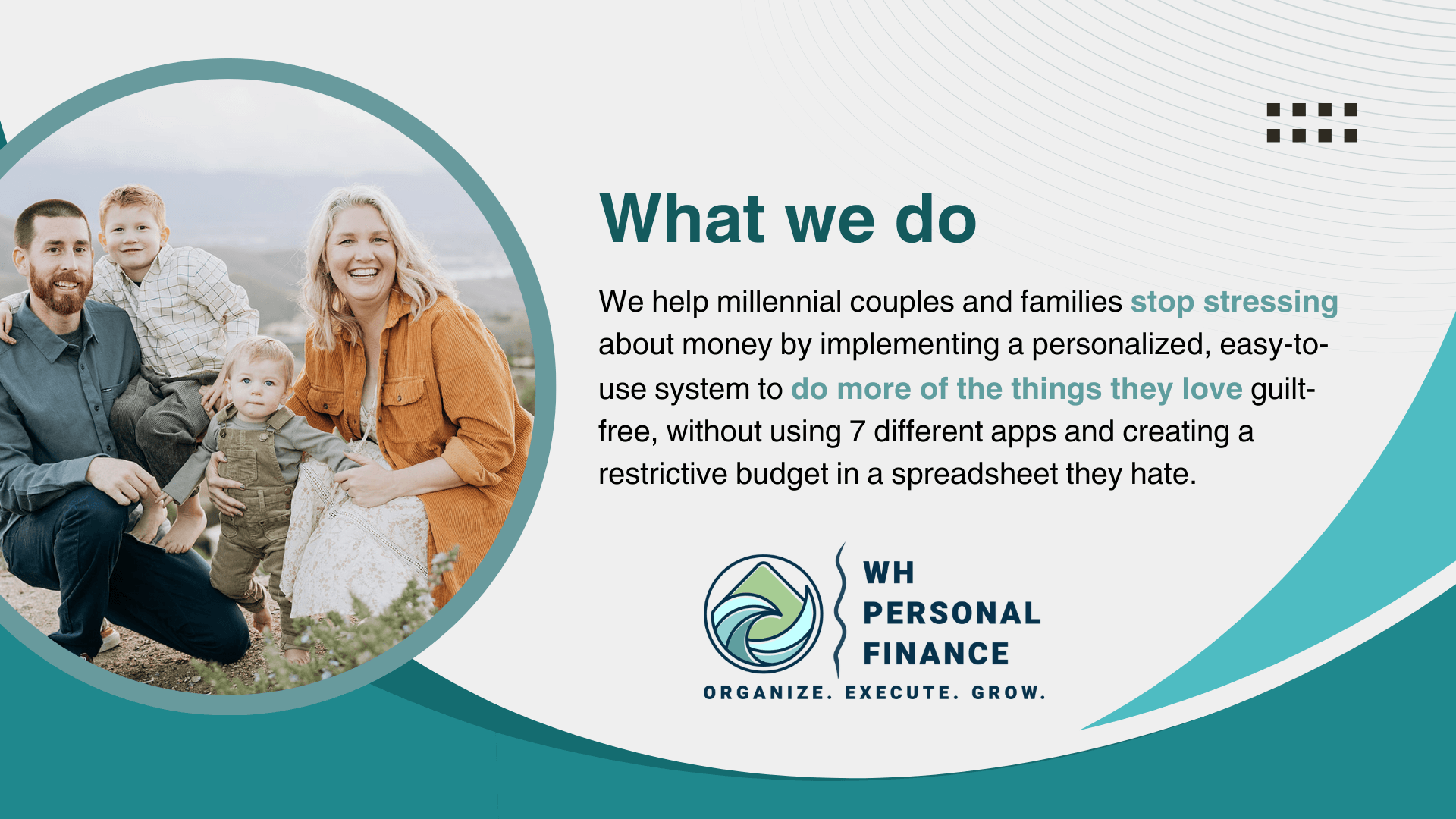

Our Mission is to help people stop stressing about money and do more of what they actually love, guilt free. We help people get all their finances organized, clarify their values and goals and create a customized plan that is easy to manage long-term and aligns values, financial goals, and living a good life.

Awesome – so before we get into the rest of our questions, can you briefly introduce yourself to our readers.

My name is Josh Williams, I’m the oldest of three from a working class family in Southern California. I’m a first generation college graduate from Cal State Univ. Monterey Bay with a bachelors in Business/Entrepreneurship. I gravitated toward Excel, data analytics, and Finance in college which would help define my path later on.

Growing up I was an extreme sports kid more than a “sportsball” kind of kid. Go carts, dirt bikes, skiing, snowboarding you name it. But being in a working class family with divorced parents sometimes meant I had to save my own money for some of the expensive toys I set my sights on. It also meant I had to be tough and work hard.

As I got older, I set my sights on becoming a welder and dreamt of owning my own welding shop while living near the beach. At the time, I was taking the bare minimum amount of credits to maintain health insurance while on my mom’s plan. I wasn’t really driven until I met my now wife, Caitlyn. She was in college in Monterey, I was in LA and just like that I had something to really work for. I went from taking (and failing) 2 classes a semester, ignoring medical debt and collections calls to taking a full course-load during the day and 4 hours of welding school at night while working weekends at a local paintball field. I completed 2 years of coursework in one semester and one summer and earned an AA in Welding Technology from my local community college. I was accepted into CSU Monterey Bay and began working as a welder while earning my business degree, by the beach with the girl of my dreams.

Things were good, but I was beginning to realize I didn’t want to be a welder for the rest of my life. Everything I ever touched was Hot, Heavy, Dirty, or Sharp and I was making $10/hr.

In school, one of my most impactful courses was Personal Financial Management which allowed me to build a solid foundation early. Soon after graduation I was working for Driscoll’s in data analytics. I sat on the advisory board for the School of Business after being invited by none other than the professor who taught my Finance and Personal Financial Management courses. We knew wanted to help the community we lived in so we became CASA’s (court appointed special advocate) for abused/neglected kids in the foster care system which both gave us new perspective and fed the “giving bug” within each of us. I also learned how systems can fail people and hard work alone wasn’t enough to get ahead.

As I built my career I also built a personal finance system that had us living within our means, fixed my credit, creatd an emergency savings account, paid down student loans and saving to buy our first home. We bought our home, got married, and worked hard to further our careers. We stuck to our financial system; 10% of our take-home was for long term savings, 20% for bad debt, 70% for living expenses, which included 5% for vacations and 5% for house projects, and 60% to live on. We thrifted a lot. We DIYed all the time. We found and used an app to track accounts and expenses and kept lifestyle creep at bay. We paid off our cars but kept saving the equivalent to our loan payments for repairs and future car purchase. As friends and family heard about how we approached our finances they passively suggested we might be able to do this for a living.

We fixed up the house, got a dog, a small camper, skied a lot, had a baby, sold our house and bought another. I was working for Santa Cruz Bicycles in analytics Caitlyn was working on her Masters… there was no time to start a business. We had built up 6 months worth of expenses in emergency funds, funded our retirement accounts, opened ROTH IRAs and a joint brokerage account then one day in 2023 I was called in to an unnamed meeting where I was part of the first round of mass layoffs. An event like this could have meant financial disaster for many but the work we had put in years prior allowed us hunker down, pull from savings and carry on. It created a decision point we decided to do the thing, make the jump and start our own business from scratch with the aim to get people setup to clear hurdles, stop stressing and do more of what they actually love in life. We aren’t trying to build an empire we are looking to help as many people as we can and live a humble life aligned with our own values.

Work hard and be nice to people.

We help our clients stop stressing about money so they can do more of what they actually love, guilt free. Organize. Execute. Grow is our tagline and our 3 step process. The dollar amounts don’t really matter much to me, what I love to see is the growth that clients feel when they understand their habits and have a solid system to improve their life.

Most people have never been taught how to manage their money. Usually, we find that they picked up on habits and biases from a very young age, both good and bad. Then in early adulthood they get a job and its suddenly like, “figure it out”, mostly on their own. To make things even harder they are faced with the social stigma of not really ever talking about money with anyone and a complete avalanche of information online to try to make sense of on their own.

We come at this from a human side first. The TV personality tough-love approach doesn’t work long term. Instead, It adds to the feelings of embarrassment and shame people feel without addressing the foundations of those feelings.

We make a point to acknowledge how hard it is to talk about your personal finances, let alone with a stranger. Testimonials from past clients have a common thread of non-judgement and trust which I’m quite proud of.

We begin with a Money Map devoid of dollar amounts on purpose. I just want to see what we are dealing with, what accounts they have, savings, credit cards, subscriptions, bills etc. This gives us a really good starting point to understand the landscape and structure people already have in place, good or bad.

Next we talk about what goals they have and the meaning behind those. That conversation leads naturally into a values discussion. Those three things; The Money Map, Goals, and Values, when nailed, make all the money and numbers discussions really easy.

People need emergency savings in place to stop the debt cycle. You need to know what you value so you can spend money on true happiness and cut out other unnecessary stuff. You need a system to track balances and spending that is quick and easy so you don’t burn a bunch of time and stress trying to figure it all out. Your spending patterns will tell a story and your values and goals will help you adjust your future patterns. Many of the elements interact with each other so we start from the ground up and meet clients where they are at. We find ourselves smack dab in between therapy and Financial Advising. We are the missing piece that keeps people in their cycles and from figuring this finance thing out. 80% of people have reported feeling like they are living paycheck to paycheck regardless of their income level. The system we help clients build is much more important than the dollar amounts associated. We help solve a bunch of small problems and let the system and its automations take the thinking and stress out. This allows people to focus their mental load on spending based on their values and goals while the rest is “set-it-and-forget-it”.

I came from a background of money stress and built a system for my household that I didn’t really realize was awesome until friends and family started telling me so. Once I realized I had built something that could really help people I realized how many people I could help and WH Personal Finance was born. I’m not trying to build an empire, I’m trying to make a humble living while helping as many people as I can.

Can you tell us about what’s worked well for you in terms of growing your clientele?

Word of mouth referrals, I really enjoy talking to people and getting to know them well. We are working on getting out into the community as much as possible. We are making connections with adjacent professionals who don’t have the system or time to help clients with personal finance. Therapists offer really good leads because money can cause so many relationship issues but many don’t dive into the money aspect with clients. The same goes with Tax professionals and Advisors on the other end of the spectrum. We jump at the chance to do vendor popups and networking events, but at the end of the day the non-judgmental, trustworthy approach is what is working best. Many people we talk to see the need and value that we offer but aren’t ready to acknowledge or make the change, yet. But when they are we will be here ready to help.

We’d love to hear the story of how you built up your social media audience?

I am still working on this one. Someone once described writers block as “creative constipation” and I couldn’t agree more. I know a lot about personal finance and how to build a system that is flexible and really easy to stick to long term but when someone asks me for 5 financial tips I find it really hard to spit out an answer. Same goes for creating social media content. I haven’t yet found my groove my posts tend to be heartfelt and showcase what I love and value most, my family. Lots of advice out there says social media is most effective when you are consistent which makes total sense intuitively but after thinking about strategy and hooks and audience I came really realized it all comes back to being consistent. Its weird how knowing something and feeling something can be so different.

Contact Info:

- Website: https://www.whpersonalfinance.com

- Instagram: @whpersonalfinance

- Facebook: WH Personal Finance

- Linkedin: Josh Williams

![]()

Image Credits

Family Pictures courtesy of Zoom Theory Photography, zoomtheory.com